Residential Property Review – July 2025

| City of London investment volumes are rising, with May hitting the highest deal count so far in 2025 | Owner-occupier demand is increasing as mortgage costs undercut commercial rents by up to 37% | Scottish commercial investment fell 20% in H1 2025, though hotels led performance and private buyers remained active |

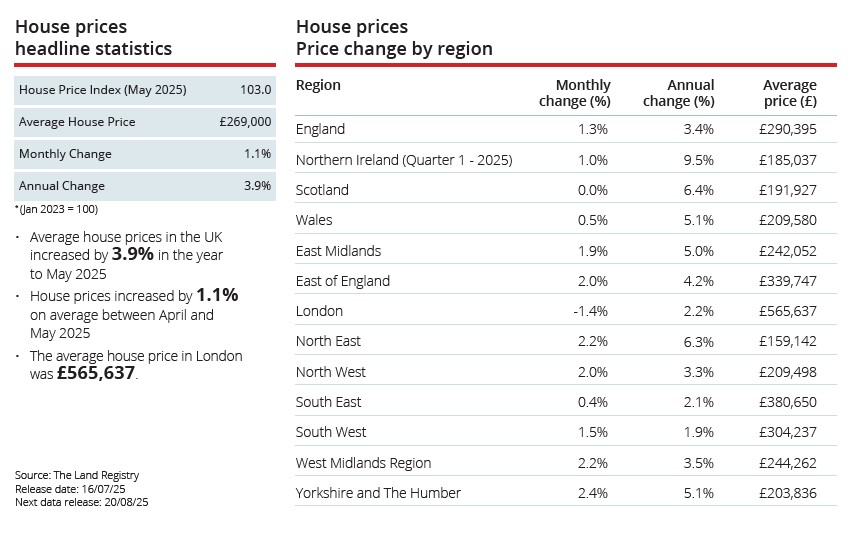

A smoother end to 2025?

The second half of the year should be smoother for the UK housing market, according to Knight Frank.

The first six months of 2025 brought some uncertainties, with Trump’s trade tariffs, ongoing geopolitical conflict and Stamp Duty changes. However, things may be looking up.

Buyer activity seems to be recovering after Stamp Duty thresholds reverted to higher levels in April. This initially caused a 37% decline in transactions; however, in May there was a smaller drop of 17%, suggesting that activity is picking up. Supply still outweighs demand, as the number of new homes for sale between January and May was 15% higher than the five-year average.

Experts believe that there will be further cuts to Bank Rate this year, which would help boost the market. However, there are concerns that the government will announce more tax rises in the Autumn Budget to create financial headroom.

Strong demand for new builds in key cities

Property Inspect reported that demand for new builds remained stable in Q2 2025.

New-build demand was 18.2% in quarter two, only 0.2% less than Q1. This stability is driven by strong performance in cities, with demand highest in Southampton, where over a third (35%) of new-build homes are sold subject to contract (SSTC). Portsmouth is second on the list with 28%, followed by Sheffield (20.6%), Glasgow (19.5%) and Bristol (19.1%).

On the other hand, demand was weakest in Swansea, where only 1.1% of new builds were under offer. The Welsh city is joined at the bottom by Liverpool, where 3% of new homes were SSTC. Aberdeen saw the largest quarterly drop in interest, where demand fell by 10%.

Commenting on the research, Siân Hemming-Metcalfe, Operations Director at Property Inspect, said, “Activity in many major cities highlights that buyers are still transacting, even in the face of higher price points”.

Decline in property flipping

The number of homes being flipped has dropped to the lowest level since 2013, according to Hamptons.

Property flipping – buying homes to renovate and quickly resell – has become less common. In Q1 2025, only 2.3% of homes sold in London had been bought within the last year, a 3.6% annual decrease. Although the average gross profit from flipping a property rose this year to £22,000, it is still below the peak of £38,000 seen in 2022. This drop is likely due to a slowdown in house price growth.

Flippers seem to be retreating from the South, with only 1.5% of homes in London resold within a year. In the capital, 23% of the average profit from flipping went towards Stamp Duty, which has likely been a deterrent for investors. Meanwhile, the North East is a popular spot, where flipped homes accounted for 4.7% of all sales in Q1.

Sales stabilising but not yet recovering

The latest report from the Royal Institution of Chartered Surveyors (RICS) suggests that the sales market is stabilising.

Buyer demand is in positive territory for the first time since December 2024. The net balance for new buyer enquiries increased to +3% in June, significant progress when compared with -22% in May. The net balance for sales agreed also improved, rising from -25% and -28% in the two previous months to -3% in June. However, these figures suggest that buyer and seller momentum is stabilising, rather than recovering.

As for the lettings market, tenant demand remained relatively flat in June, with a net balance of -2%. A quarter (24%) of those surveyed expected rents to rise in the next three months, down from 43% of respondents in May.

RICS Head of Market Research and Analysis, Tarrant Parsons, commented, “Confidence in the market remains somewhat delicate, with economic uncertainty at both the domestic and global level still seen as a potential headwind. “

(All details are correct at the time of writing 16/07/25)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission